Municipal bonds, also known as muni bonds, are a crucial financial instrument utilized by California school and community college districts in the construction and modernization of facilities and infrastructure. When districts issue their muni bonds, they are sold by underwriters to investors. But how do investors looking to purchase municipal bonds decide which muni bonds to buy? With so much municipal debt entering the market every day along with access to municipal bonds in the secondary market, how are investors able to compare them? Credit ratings are a key tool used by investors when evaluating which municipal bonds to purchase. Tony Hsieh of Keygent LLC delves into credit ratings, which factors are considered, and their impact on interest rates.

What are Credit Ratings?

Credit ratings for municipal bonds serve as a crucial indicator for investors seeking to evaluate the risk associated with a particular muni bond issuance. These ratings provide an independent assessment of a California school or community college district’s ability to meet its financial obligations. For investors looking to purchase municipal bonds, credit ratings serve as a reliable metric to assess the likelihood of timely interest and principal payments and any potential risk of defaults. Higher credit ratings indicate a lower risk of default, providing assurance to investors who are looking for lower risk investments. Credit rating agencies use a grading system that serves as a guide for investors to make informed decisions based on their risk tolerance and investment objectives.

Given that school and community college districts are vastly different from one another, each with its unique economic and financial landscape, credit ratings serve as a standardized scale for investors to gauge the financial strength and stability of various issuing districts. This uniformity allows investors to efficiently evaluate and fairly compare the risk of municipal bonds from varying entities. Ultimately, credit ratings provide investors with a transparent and standardized measure to navigate the municipal bond market.

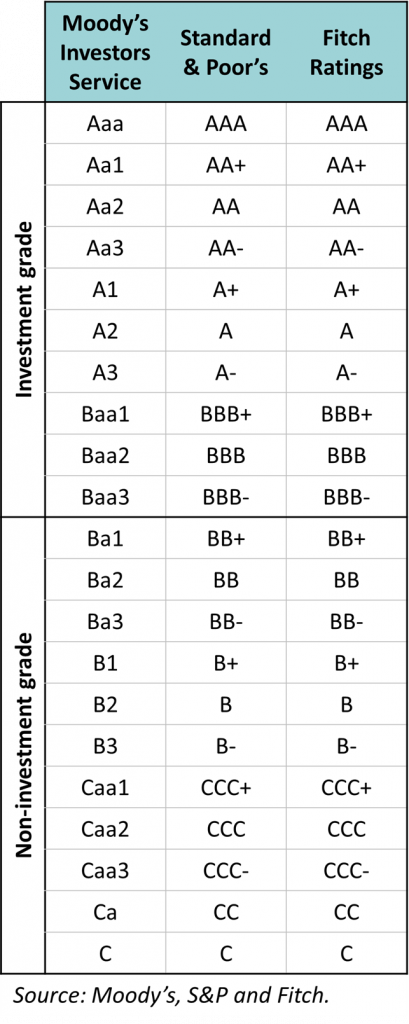

There are three primary rating agencies that assess the creditworthiness of municipal bonds, each with its own methodology and criteria. The three rating agencies are Moody’s Investors Service, Standard & Poor’s, and Fitch Rating. Moody’s Investors Service was founded in 1909 and uses a rating scale ranging from Aaa, the highest quality, to C, the lowest quality. Standard & Poor’s was founded in 1860 and uses a scale ranging from AAA, the highest quality, to C, the lowest quality. Fitch Ratings was founded in 1913 and also uses a scale ranging from AAA, the highest quality, to C, the lowest quality. The rating scale used by each respective credit rating agency is as follows:

An in-depth description of each credit rating above can be found at the respective credit rating agency’s website.

Factors That Influence Your Municipal Bond Credit Ratings

Tony Hsieh of Keygent explains, “Credit rating agencies evaluate the following factors to determine the creditworthiness of municipal bonds: local economy, district finances, district management, and district debt.” An understanding of these factors helps investors make informed decisions on which municipal bond issuances to purchase.

- Local Economy: The local economic environment plays a significant role in determining credit ratings. Agencies assess factors such as employment rates, income levels, home sales and assessed value to gauge the local economy. Assessed value of property within a district directly influences its property tax revenue, which is a significant revenue source for local governments. Credit rating agencies consider this revenue stream as part of their assessment of a district’s ability to meet its financial obligations. Higher assessed property values generally contribute to a larger property tax base, generating more property tax revenue for the issuing district. A strong and stable property tax base is often viewed positively, as it enhances a district’s ability to service its municipal bond debt and fulfill other financial obligations. Conversely, if a district has a declining or unstable assessed property value, it may raise concerns for credit rating agencies. Home sales are used as an indicator for potential future growth in assessed value by credit rating agencies. Strong economic fundamentals can positively impact credit ratings, while economic challenges may result in lower ratings.

- District Finances: Credit rating agencies analyze historical budgetary performance along with projected budgets to assess a district’s ability to balance revenues and expenditures. Consistent budget surpluses demonstrate fiscal responsibility, whereas continued budget deficits may raise concerns. A strong budgetary performance contributes positively to credit ratings, reflecting a district’s financial stability. Additionally, population trends and demographic factors are considered when assessing a district’s finances. Since districts are largely funded based on their enrollment and attendance, rating agencies examine population stability, demographic shifts, and enrollment projections that may impact future revenue for a school or community college district. Districts experiencing positive demographic trends may receive higher credit ratings due to the potential future funding growth.

- District Management: Effective financial management is crucial for maintaining a favorable credit rating. Sound fiscal policies, conservative budgeting practices, and prudent debt management contribute positively to credit rating assessments. California school and community college districts with strong financial management practices are considered to be better positioned to weather economic uncertainties and meet their financial obligations.

- District Debt: The amount of outstanding debt and the structure of that debt are key considerations in credit rating assessments. Credit rating agencies evaluate the debt burden relative to a California school and community college district’s ability to meet existing obligations. Well-structured debt with manageable repayment terms is viewed more favorably, while high debt levels may lead to lower credit ratings. Additionally, debt that is a repaid from a district’s general fund, or operating budget, may be viewed as a liability by a credit rating agency and can negatively impact credit ratings.

Keygent LLC: What to Expect When Seeking a Credit Rating for Your Muni Bonds

Typically, when issuing municipal debt, part of the issuance process involves California school and community college districts to speak with at least one of the three previously mentioned credit rating agencies. The number of credit ratings a district may seek is typically dependent on the size of the financing. Investors may be comfortable with only one credit rating for smaller financings while for larger financings they often prefer two credit ratings. Districts can consult with their municipal advisor to help determine which and how many agencies they should seek a rating from for their muni bonds.

Once a rating agency, or agencies, have been identified, typically a district’s municipal advisor will coordinate the date and time for district officials and members of the financing team to speak with analysts from the rating agency. Credit rating meetings can be done in-person, virtually or by phone, whichever option is best suited for the district and financing team. At the meeting, the district has an opportunity to discuss and present information about its local economy, district finances, district management and district debt as well as answer any questions. Following the meeting, the credit rating analysts will meet with an internal committee at their rating agency. That committee will then deliberate on a credit rating based on the previously mentioned factors. Once a rating has been decided, a credit rating report will be shared with the district and their financing team for any factual comments before it is made public information. California school and community college district credit ratings can be found on each of the respective credit rating agency’s website, if they have a rating from the agency.

Credit Ratings Received & Potential Updates

Once California school and community college districts receive their credit rating, it does not mean that the rating will remain unchanged for the life of the municipal bonds. Tony Hsieh of Keygent LLC notes, “Credit rating agencies periodically review and update their assessments on a district’s municipal bonds based on changes in economic conditions, financial management, and other relevant factors.” Credit rating surveillances for municipal bonds are undertaken by credit rating agencies to continually monitor the creditworthiness of municipal issuers and their bonds. This surveillance typically involves a questionnaire or phone call to receive updates on key economic indicators, budgetary performance as well as an assessment of any material changes that could impact the credit quality of the bonds. Credit rating agencies aim to provide timely information to investors by identifying emerging risks or improvements in the financial health of districts.

Credit ratings can sometimes be upgraded. An upgrade in a municipal bond’s credit rating signals improved creditworthiness and perceived reduction of risk. This may result from strong budget performance, economic growth, or successful debt reduction. Upgrades often lead to lower borrowing costs for future municipal bond issuances and increased demand from investors seeking higher-quality muni bonds. In other instances, credit ratings may be downgraded. A downgrade indicates a deterioration in credit quality. Factors such as economic challenges, weaker than expected budgetary performance, or increased debt levels can trigger downgrades. Downgraded bonds may result in higher borrowing costs for future municipal bond issuances and may experience less investor demand during the bond sale. In some instances, credit ratings will not be upgraded or downgraded but may receive an outlook on the rating. An outlook typically can be positive or negative. Typically, a positive outlook is a signal from credit rating agencies that a district’s rating may be upgraded in the next two years, while a negative outlook is a signal that a district’s rating may be downgraded in the next two years. Rating or outlook changes can have an impact of the overall borrowing cost of municipal bonds for a district.

Impact of Credit Ratings on Borrowing Costs

The credit ratings assigned to municipal bonds can have a significant impact on the borrowing costs municipal bonds issued by California school and community college districts. A higher credit rating, indicating a lower perceived risk of default, allows districts to issue a financing with more favorable interest rates. Investors view higher-rated bonds as safer investments, demanding lower yields due to the perceived lower risk of the investment. This may translate to lower borrowing costs for the issuing district. As a result, districts with strong credit ratings may benefit from having access to cost-effective capital, enabling them to fund essential projects and infrastructure improvements more efficiently.

Conversely, lower-rated muni bonds may result in higher borrowing costs for a district. Investors typically demand higher yields to compensate for the increased credit risk associated with these municipal bonds. The demand for higher yields results in higher interest rates resulting in a higher overall borrowing cost for the municipal bonds. The relationship between credit ratings and borrowing costs highlights the importance of maintaining strong finances and prudent financial management by California school and community college districts.

In addition to influencing interest rates, credit ratings also impact the demand for municipal bonds in the market. Investors seeking stable and secure investments are more likely to favor higher-rated bonds, leading to increased demand. This heightened demand can further contribute to lower borrowing costs for well-rated school or community college districts. Alternatively, lower-rated bonds may face reduced demand, resulting in the need to offer higher interest rates to attract investors. The synergy between credit ratings, borrowing costs, and market demand highlights the crucial role that credit ratings have in shaping the financial landscape for California school and community college districts.

Municipal bond credit ratings are an important part of muni bond issuances for investors and California school and community college districts alike, offering insight into the creditworthiness of bond issuances. Understanding the factors influencing credit ratings, the major rating agencies, and the implications of rating changes empowers districts to make prudent financial decisions to achieve the lowest borrowing cost for their future debt issuances. With the help of a municipal advisor, districts do not need to navigate this process alone and can have a professional guide them through the credit rating process.

Keygent LLC is a municipal advisory services firm located in El Segundo, California. Keygent has experience with assisting California school and community college districts with the issuance of their municipal debt and seeking credit ratings during the process. If you would like to learn more, please visit www.keygentcorp.com.

{kind=link}